As the April 15 tax deadline approaches, CPAs, EAs, and accounting firms must ensure their clients are well-prepared for a smooth and timely filing process. With tax laws constantly evolving and last-minute filings increasing the risk of errors, having a structured approach can help prevent unnecessary penalties and ensure compliance.

To assist in this critical period, here are key strategies to prepare and file tax returns efficiently while optimizing deductions and mitigating common errors.

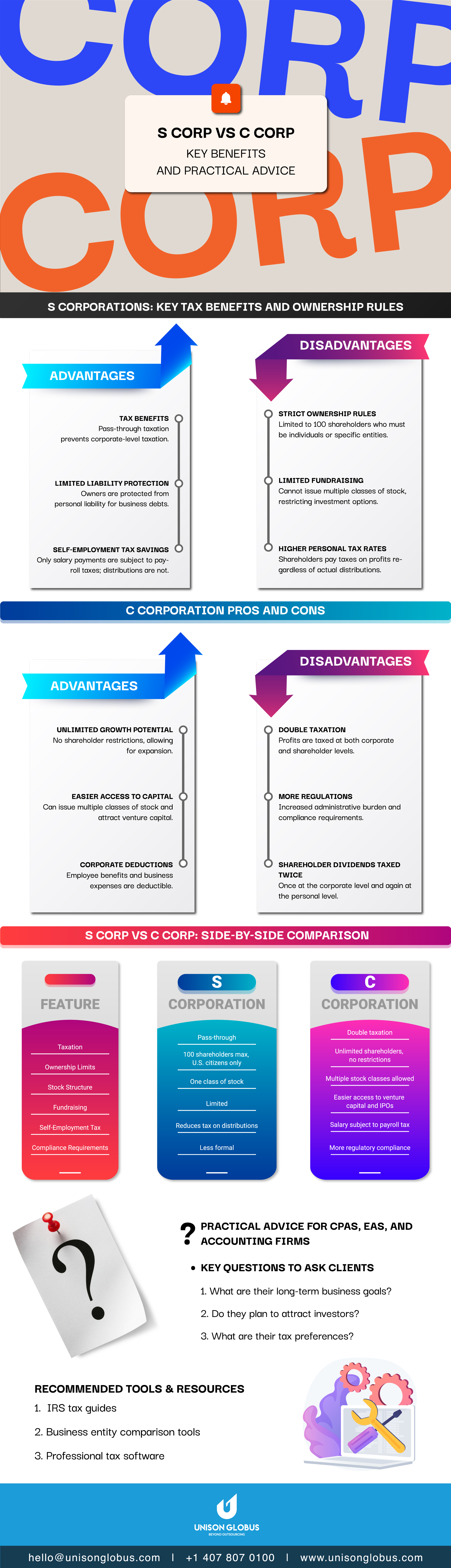

01 #1. Gather Essential Documents Early

One of the primary reasons for tax return delays is missing documentation. Encourage clients to compile the necessary forms, including:

- Income Statements: W-2s for employees, 1099s for independent contractors, and other income-related documents.

- Expense Records: Receipts for deductible business expenses, home office costs, medical expenses, and charitable contributions.

- Previous Tax Returns: Reviewing past filings ensures consistency and helps identify potential deductions or credits.

- Investment and Retirement Contributions: 1099-INT, 1099-DIV, and Form 5498 for IRA contributions.

Having these documents ready early streamlines the filing process, reducing the likelihood of last-minute stress.

02 #2. Leverage E-Filing for Speed and Accuracy

Encourage clients to opt for electronic filing (e-filing), which offers several advantages:

- Reduces Errors: E-filing software performs automated calculations, minimizing the risk of human errors.

- Provides Immediate Confirmation: Clients receive instant acknowledgment that their tax return has been submitted.

- Faster Refunds: The IRS processes electronically filed return more quickly, especially if direct deposit is chosen.

The IRS provides Free File for taxpayers earning $84,000 or less, enabling them to e-file at no cost.

03 #3. Verify Personal and Financial Information

Even minor errors can lead to tax return rejections or processing delays. Double-check:

- Social Security numbers for accuracy.

- Legal names matching IRS and Social Security Administration records.

- Bank details for direct deposit refunds.

Mistakes in these areas can delay refunds or result in notices from the IRS.

04 #4. Maximize Deductions and Credits

Help clients minimize their tax liability by ensuring they take full advantage of available deductions and credits:

- Business Deductions: Home office expenses, business travel, professional development costs, and software subscriptions.

- Education Credits: American Opportunity Credit and Lifetime Learning Credit for eligible education expenses.

- Retirement Contributions: Maximizing IRA and 401(k) contributions can lower taxable income.

- Health Savings Account (HSA) Contributions: Tax-deductible contributions can reduce taxable income.

Accurate record-keeping and documentation are essential to substantiate these claims in case of an IRS audit.

05 #5. Avoid Common Filing Mistakes

Mistakes can result in audits, penalties, or delayed refunds. The most frequent errors include:

- Math miscalculations or incorrect figures.

- Incorrect filing status (e.g., filing as “Single” instead of “Head of Household” when eligible).

- Failing to sign and date paper returns (electronic filings require a PIN instead).

Using professional tax software or consulting with a tax expert significantly reduces the likelihood of errors.

Hire expert tax professionals to streamline

your tax preparation and ensure compliance.

Unison Globus delivers precision-driven tax solutions tailored for CPAs, EAs, and accounting firms. Hire Unison Globus today for seamless, error-free tax filing! Get in touch now

06 #6. Consider Filing an Extension if Needed

If a client cannot file their return by April 15, filing an extension can provide additional time to prepare:

- Submit Form 4868: This application grants an automatic six-month extension until October 15.

- Understand Tax Payments: An extension to files does not mean an extension to pay. Any taxes owed should be estimated and paid by April 15 to avoid interest and penalties.

While extensions offer flexibility, filing sooner helps clients avoid last-minute stress and potential IRS scrutiny.

07 #7. Stay Informed About IRS Resources and Tax Law Changes

The IRS offers valuable resources to help taxpayers file accurately:

- Interactive Tax Assistant for answering common tax law questions.

- “Where’s My Refund?” tracking tool to monitor refund status.

- Special assistance, including extended hours at select locations, to support last-minute filers (IRS newsroom).

Additionally, staying updated on recent tax changes ensures compliance and maximizes tax-saving opportunities.

08 #8. Be Cautious of Tax Scams

With the rise of digital fraud, warn clients about common tax scams:

- Phishing Emails and Phone Calls: The IRS does not initiate contact via email, text, or social media to request financial details.

- Fake IRS Representatives: Scammers impersonate IRS agents to demand immediate payments. Always verify directly through the official IRS website.

- Identity Theft: Encourage clients to use secure passwords and enable multi-factor authentication when accessing tax filing software.

Staying vigilant helps clients protect their financial data and prevent fraud.

Key Takeaways for CPAs, EAs, and Accounting Firms

- Help clients file early to avoid penalties and maximize refunds.

- Leverage e-filing and automation for accuracy and efficiency.

- Review tax deductions and credits carefully to optimize tax savings.

- Monitor IRS updates to stay compliant with new regulations.

- Advise on tax payment options to prevent financial strain for clients.

09 #9. Manage Tax Payments Wisely

For clients who owe taxes, planning for payments is essential:

- Electronic Payment Options: IRS Direct Pay and Electronic Federal Tax Payment System (EFTPS) allow secure, instant payments.

- Installment Agreements: If unable to pay in full, setting up a payment plan with the IRS can prevent further penalties.

- Estimated Tax Payments: Self-employed individuals should make quarterly estimated payments to avoid underpayment penalties.

Proper tax planning reduces financial strain and ensures compliance.

10 #10. Maintain Proper Records for Future Reference

Encourage clients to retain copies of tax returns and support documents for at least three years:

- Helps resolve discrepancies with the IRS if questions arise.

- Provides documentation for financial planning and loan applications.

- Serves as a reference for next year’s filing.

Organized record-keeping simplifies future tax filings and ensures compliance with audit requirements.

Final Thoughts:

Partner with Experts for Hassle-Free Tax Filing

The tax season can be overwhelming for businesses and individuals alike. By adopting proactive filing strategies, leveraging available IRS resources, and staying vigilant against common pitfalls, CPAs, EAs, and accounting firms can help their clients navigate tax season with confidence.

At Unison Globus, we specialize in providing outsourced tax preparation services tailored for North America-based accounting firms. Our expert team ensures accurate, timely, and compliant tax filings, freeing you to focus on strategic financial advising for your clients.

Looking for expert tax preparation and compliance solutions? Contact Unison Globus today to streamline your tax season and maximize your efficiency.

Pro Tips - For a Hassle-Free Tax Filing Process

Income-related documents: W-2s, 1099s, K-1s, and investment statements

Income-related documents: W-2s, 1099s, K-1s, and investment statements

01. India:

01. India:  02. Philippines:

02. Philippines:  03. Vietnam:

03. Vietnam:  04. Poland:

04. Poland:  05. South Africa:

05. South Africa:  06. Malaysia:

06. Malaysia:  07. Mexico:

07. Mexico: